Europe is building a regulatory architecture that will make product-level carbon data essential on a defined timeline starting in 2027. For manufacturers, this means that the products they sell will need to start carrying a product carbon footprint (PCF). Not because they are directly affected by regulations, but because the companies they sell to, or the companies their customers sell to, are.

Regulations today tend to focus on consumer-facing industries. That is creating a ripple effect: B2C companies under scrutiny are passing the demand for carbon transparency straight down their supply chains, making emissions data a hard requirement in procurement decisions and RFPs.

Enter PCFs. A PCF quantifies the greenhouse gas emissions associated with a specific product across its lifecycle. It is the unit of measurement that makes scope 3 commitments actionable. PCFs turn a commitment to "reduce scope 3 emissions" into something a procurement team can actually put in a contract, and a regulatory requirement for "verified, product-level carbon data" into a number an auditor can check.

By mandating scope 3 reporting for large companies and raising the bar on data quality, CSRD creates a cascade of pressure that flows down supply chains from the companies directly in scope, to their suppliers, to their suppliers' suppliers. In conversations we’ve had with manufacturers, they told us that their “competitors now have their PCFs ready. The clients, the big ones, are really pushing on it.” As a consequence, manufacturers that cannot provide their customers with verified PCF data will increasingly find themselves on the wrong side of procurement decisions.

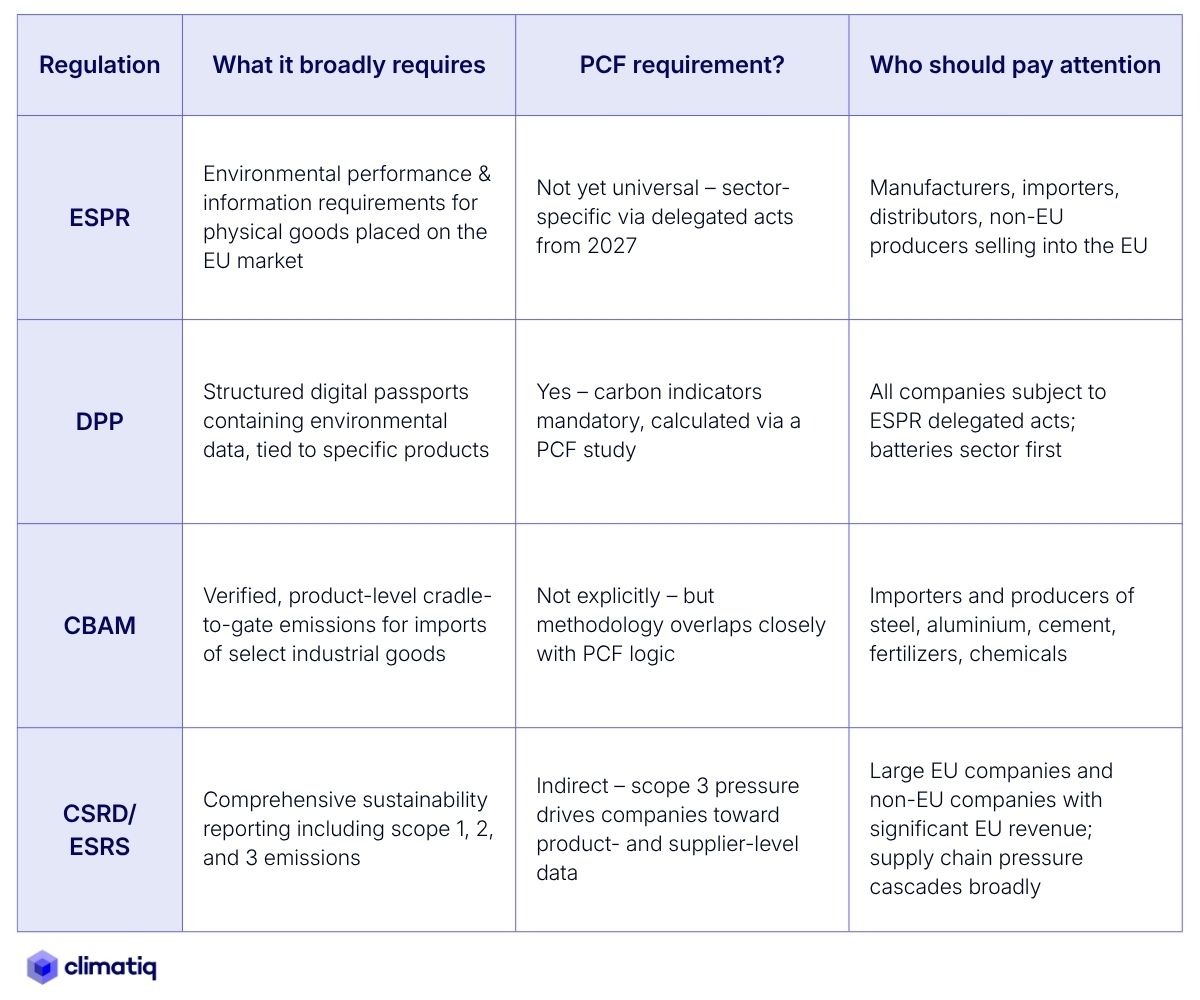

The Ecodesign for Sustainable Products Regulation (ESPR) is the cornerstone of Europe's product sustainability framework. It covers almost all physical goods placed on the EU market and applies to manufacturers, importers, distributors, and non-EU producers selling into the EU.

PCFs are explicitly listed within ESPR as an example of environmental information that may be required. ESPR does not yet mandate PCFs universally, but it creates the legal framework that will make them unavoidable for many sectors in the next few years.

ESPR replaces the Ecodesign Directive, which was largely limited to energy-related products and energy efficiency requirements. The new regulation dramatically expands scope, moving from energy performance to a broad set of environmental sustainability criteria, including carbon footprint, resource use, recyclability, and durability.

ESPR is being rolled out in phases, with delegated acts specifying detailed requirements, such as PCF rules, calculation methodology, format, and verification, for each product group. The current priority sequence covers:

Once a product group receives a delegated act, companies in that category face binding requirements on what PCF data they must calculate, how it must be verified, and how it must be communicated. Delegated acts for priority sectors are expected to begin taking effect from 2027 onwards.

The enforcement mechanism for ESPR is the Digital Product Passport (DPP). DPPs are structured, machine-readable records that travel with products and contain verified environmental data, including carbon footprint information. Carbon-related indicators within DPPs will be mandatory for in-scope products, calculated through a PCF. Batteries are the first live test case, with DPP requirements already advancing through regulatory development. Read more in our DPP deep-dive.

The Carbon Border Adjustment Mechanism (CBAM) takes a different approach to the same underlying challenge. Rather than setting product performance standards, it attaches a carbon price to imports of carbon-intensive goods entering the EU, ensuring that foreign producers face equivalent carbon costs to their EU competitors.

CBAM currently covers iron & steel, aluminium, cement, fertilizers, electricity, and hydrogen. The requirement is for verified, product-level cradle-to-gate carbon emissions—which is exactly the same scope that a PCF addresses.

CBAM does not use the term "PCF" explicitly, nor does it mandate a specific PCF methodology. But the data it requires is functionally equivalent to a PCF. Companies that have already invested in PCF capabilities will find CBAM compliance significantly easier than those starting from scratch.

CSRD is not a direct PCF mandate, but it is one of the most powerful indirect drivers of PCF adoption in the market today, and will hit manufacturers whether they’re in scope or not.

By requiring large companies to report scope 3 emissions under the European Sustainability Reporting Standards (ESRS), CSRD forces organizations to confront the quality of their supply chain carbon data. Most companies currently rely on spend-based emissions estimates—at least in the early stages—which uses financial spend as a proxy for emissions. It is fast and cheap, but it lacks product-level precision and transparency. As it relies on industry averages, the spend-based method is not suited for granular analysis or actioning reductions.

As reporting scrutiny increases, companies are expected to migrate away from spend-based estimates towards primary, supplier-specific data, which eventually leads to PCFs. Unlike the spend-based method, PCFs are calculated with activity data that is focused on a specific product or project to provide more nuanced estimates. We’ve already seen this transition underway at the leading edge of European industry in conversations with major companies. Don’t just take our word for it: DuPont and BT are just some of the major players who have begun explicitly requiring PCF data from suppliers as a condition of doing business, embedding CO2 data availability as a KPI in their RFPs.

The implications for supply chains are significant. A tier-1 supplier to an in-scope CSRD company faces direct commercial pressure to provide PCFs. That pressure then spreads to tier-2 suppliers, and so on. The regulatory obligation may sit with large companies, but the practical demand for PCF data reaches far deeper into the supply chain—right down to the manufacturers of the raw products.

Act now if you are in a sector covered by early ESPR delegated acts (batteries, textiles, electronics), if you export to the EU and your products fall under CBAM, or if you are a direct supplier to large companies already in scope for CSRD. In these cases, PCF requirements are arriving on a defined schedule, and building PCF capabilities takes time.

Prepare now if you are in sectors further down the ESPR priority list, or if your exposure is currently indirect through customer pressure rather than direct regulation. The window to build internal capabilities, establish data collection processes, and develop supplier engagement programs is narrowing. Plus, the earlier that manufacturers start to put these workflows in place, the easier the process becomes.

Manufacturers who don’t prepare now will start losing deals. As leading companies in every sector embed PCF requirements into procurement processes, suppliers without verified carbon data are going to find themselves unable to compete for contracts.

A practical timeline to keep in mind:

Europe is setting the pace, but it is not acting alone. Policymakers and industry bodies in East Asia, Australia, Japan, and South Korea are closely tracking Europe's regulatory architecture and beginning to develop frameworks of their own. The SEC's climate disclosure rules in the US, while contested, reflect the same underlying direction of travel.

For manufacturers investing in PCF capabilities today, the competitive advantage extends well beyond EU compliance. Companies that build robust, auditable PCF programs now will be positioned to meet requirements as they emerge across global markets, turning an initial investment into a durable differentiator. Without it, more and more customers will start switching suppliers, and the number of lost deals will begin piling up.

.svg)